Drawdowns of student loans decreased in January year on year

28.2.2024 10:00:00 EET | Suomen Pankki | Press release

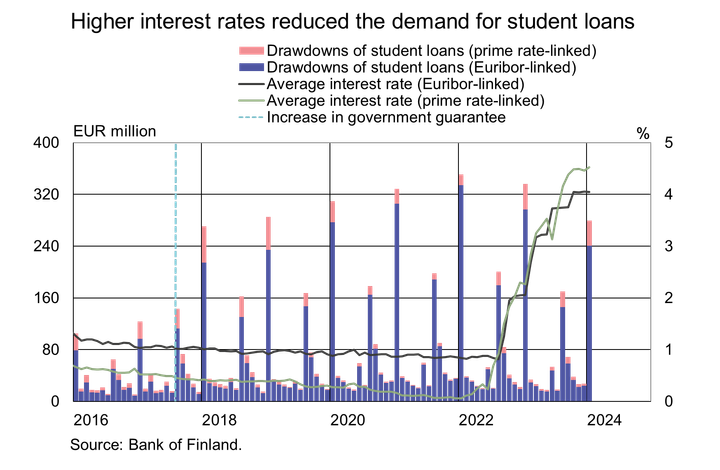

In January 2024,1 drawdowns of student loans totalled EUR 279 million, representing a decline of 17% on the corresponding period last year. This was the lowest level of new student loan drawdowns in January since 2018. The average interest rate on student loans drawn down in January 2024 was 4.46%, which was 2.22 percentage points higher than in January last year. This is the highest average interest rate on new student loan drawdowns since November 2008.

Euribor-linked loans accounted for 86% of all student loan drawdowns, and the average interest rate on these loans was 4.52%. Banks’ own reference rates have become more popular in new student loan drawdowns. In January 2024, 14% of new student loan drawdowns were linked to prime rates, or banks’ own reference rates, as opposed to 5% in January 2022. The average interest rate on new drawdowns linked to banks’ own reference rates (4.04%) was slightly lower than that on Euribor-linked ones.

The rapid growth of the student loan stock has levelled off. At the end of January 2024, the stock of student loans amounted to EUR 6.2 billion, and its annual growth rate was 4.0%. The last period with slower year-on-year growth was September 2011. While the stock has grown rapidly in recent years, the annual growth rate has been in a stable decline due to decreasing drawdowns and student loan compensations paid by Kela.2 The stock of student loans has more than doubled since the student aid reform in 2017. In addition to the larger loan instalments following the reform, the student loan stock has also been boosted by an increase in the number of borrowers.3

Loans

New drawdowns of housing loans by Finnish households amounted to EUR 0.8 billion in January 2024, which is EUR 40 million less than in the same period a year earlier. Buy-to-let mortgages accounted for EUR 90 million of the new housing loan drawdowns. The average interest rate on new housing loans decreased from December, to stand at 4.36% in January. At the end of January 2024, the housing loan stock totalled EUR 106.4 billion, and its year-on-year growth amounted to -1.5%. Buy-to-let mortgages accounted for EUR 8.6 billion of the housing loan stock. At the end of January, Finnish households’ loan stock included EUR 17.8 billion of consumer credit and EUR 17.7 billion of other loans.

In January, Finnish non-financial corporations drew down new4 loans worth EUR 1.8 billion, including EUR 490 million of housing corporation loans. The average interest rate on new corporate-loan drawdowns rose from December, to 5.58%. At the end of January, the stock of loans granted to Finnish non-financial corporations stood at EUR 107.1 billion, whereof housing corporation loans accounted for EUR 44.0 billion.

Deposits

At the end of April 2024, Finnish households’ aggregate deposit stock totalled EUR 108.2 billion, and the average interest rate on these deposits was 1.25%. Overnight deposits accounted for EUR 68.8 billion and deposits with agreed maturity for EUR 11.6 billion of the total deposit stock. In January, Finnish households made new agreements on deposits with agreed maturity in the amount of EUR 1,470 million, at an average interest rate of 3.40%.

For further information, please contact:

- Usva Topo, tel. +358 9 183 2056, email: usva.topo(at)bof.fi.

- Tuomas Nummelin, tel. +358 9 183 2373, email: tuomas.nummelin(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on 2 April 2024.

Related statistical data and graphs are also available on the Bank of Finland website: https://www.suomenpankki.fi/en/statistics2/.

1 The spring semester loan instalment became available for drawdown in January.

2 In 2022, student loan compensations approximately EUR 87.8 million, and in 2015–2021 they totalled approximately EUR 226.5 million (in Finnish).

3 According to statistics published by the National Pensions Institute Kela, the number of persons with student debt amounted to 525,000 during the academic year 2022–2023, whereas the number was 63,000 lower three years earlier.

4 Excl. overdrafts and credit card credit.

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Better now to keep interest rates unchanged24.7.2026 13:10:00 EEST | Blog

You don’t have to be much of a fortune-teller to note that there is continuing uncertainty both in the Finnish summer and in the global economy. On a chilly summer’s day like the one we’ve experienced this week, a Finn can simply stoke a fire in the sauna stove – problem solved. Unfortunately, there is no silver bullet to economic uncertainty. Rather than fanning the flames, we need to keep a cool head.

Utkasten till framtida eurosedlar har offentliggjorts – Ville Tietäväinens förslag har gått vidare23.7.2026 17:56:14 EEST | Nyheter

Ett förslag från Finland har gått vidare i formgivningstävlingen för de framtida eurosedlarna. Ville Tietäväinens sedelserie baserar sig på temat ”Floder och fåglar”. De förslag som gick vidare valdes ut genom en formgivningstävling i hela Europeiska unionen.

Uudet euroseteliluonnokset julki – Ville Tietäväisen ehdotus jatkoon23.7.2026 17:56:14 EEST | Uutinen

Suomalainen ehdotus on päässyt jatkoon uusien eurosetelien ulkoasukilpailussa. Ville Tietäväisen setelisarja perustuu teemaan ”Joet ja linnut”. Jatkoon päässeet ehdotukset valittiin Euroopan unionin laajuisessa suunnittelukilpailussa.

ECB avslöjar vilka förslag till nya sedlar som har gått vidare och inleder undersökning bland allmänheten23.7.2026 17:18:18 EEST | Pressmeddelande

ECB avslöjar vilka tio sedelutformningsförslag som har gått vidare i tävlingen Européer bjuds in att tycka till i en webbenkät öppen till och med 21 september ECB-rådet förväntas välja vinnarförslaget runt årsslutet

EKP paljastaa ehdotukset uusiksi euroseteleiksi ja käynnistää kyselytutkimuksen23.7.2026 17:18:18 EEST | Tiedote

EKP julkistaa suunnittelukilpailussa jatkoon päässeet kymmenen ehdotusta uuden eurosetelisarjan ulkoasuksi Eurooppalaisten mielipiteitä halutaan kuulla verkkokyselyssä, joka on avoinna 21.9.2026 asti EKP:n neuvoston on tarkoitus valita ehdotuksista setelisarjan lopullinen ulkoasu vuoden lopulla

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom