Deposits with agreed maturity increased in September from a year earlier

28.10.2024 10:00:00 EET | Suomen Pankki | Press release

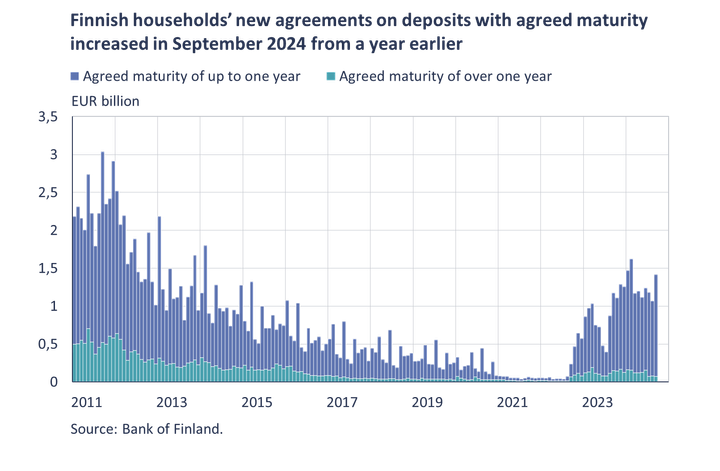

In September 2024, Finnish households concluded a higher number of new agreements on deposits with agreed maturity than a year earlier. New agreements totalled EUR 1.4 billion, an increase of EUR 0.2 billion from September 2023. The increase was also reflected in the stock of these deposits (EUR 14.9 billion), which grew in September at an annual rate of 64.5%. The growth rate was nevertheless slower than in the previous month.

The majority of households’ deposits with agreed maturity are with a maturity of up to one year. In September 2024, new deposits of this maturity type accounted for 95% of all new agreements on deposits with agreed maturity – the largest share in monthly terms in the history of the data series. Of the stock of agreed maturity deposits, 65% are with a maturity of up to 1 year and 35% with a maturity of over 1 year.

The interest rates on households’ new agreements on deposits with agreed maturity have declined for three months. In September 2024, the average interest rate was 3.29%, compared with the near-term peak of 3.56% recorded in June. With falling market rates, the interest rates on deposits with longer maturities have fallen below those on deposits with shorter ones. In September, the interest rate on new deposits with an agreed maturity of up to one year was 3.3% and on deposits with an agreed maturity of over one year 3.23%. The average interest rate on the stock of agreed maturity deposits also fell slightly in September, to 3.19%.

Households usually conclude a higher number of agreements on deposits with agreed maturity when these are remunerated at higher interest rates. However, the most recent interest rates peaks have not fuelled agreed maturity deposits as in the past. In the history of the data series, the largest monthly volume of new agreed maturity deposits has been in October 2008, when households[1] made EUR 6.5 billion worth of new agreements in this deposit category, with an interest rate of 5.04%. The stock of agreed maturity deposits also reached its all-time peak during the same period, standing 73% above the September 2024 level, at EUR 25.7 billion. However, along with agreed maturity deposits, various types of deposits that are redeemable at notice have also become more common. In September, the stock of these deposits stood at EUR 29.0 billion, and the average interest rate on the deposit stock was 2.36%.

Loans

Finnish households drew down new housing loans in September 2024 to a total of EUR 1.1 billion, the same as in September a year earlier. Of the total, buy-to-let mortgages accounted for EUR 110 million. The average interest rate on new housing loans fell from August, to 3.71%. At the end of September 2024, the stock of housing loans stood at EUR 105.8 billion, and the annual growth rate of the loan stock was a negative -0.8%. Buy-to-let mortgages accounted for EUR 8.7 billion of the housing loan stock. At the end of September, Finnish households’ loan stock comprised EUR 17.9 billion in consumer credit and EUR 17.6 billion in other loans.

Drawdowns of new loans[2] by Finnish non-financial corporations in September totalled EUR 2.3 billion, of which EUR 410 million was to housing corporations. The average interest rate on the new drawdowns was down on August, at 4.83%. At the end of September, the stock of loans granted to Finnish non-financial corporations stood at EUR 108.1 billion, of which loans to housing corporations accounted for EUR 44.9 billion.

Deposits

At the end of September 2024, the stock of Finnish households’ deposits stood at EUR 110.7 billion, at an average interest rate of 1.33%. Overnight deposits accounted for EUR 66.8 billion of the deposit stock.

For further information, please contact:

Olli Tuomikoski, tel. +358 9 183 2925, email: olli.tuomikoski(at)bof.fi

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi

The next news release on money and banking statistics will be published at 10:00 on 29 November 2024.

Related statistical data and graphs are also available on the Bank of Finland website: https://www.suomenpankki.fi/en/statistics/.

[1] The figures for 2008 also include data on non-profit institutions serving households. However, these volumes have been relatively low compared with new agreements by households.

[2] Excl. overdrafts and credit card credit.

Links

Bank of Finland

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

BOFITs prognos: Rysslands ekonomiska tillväxt 2026 ligger kvar på fjolårsnivån30.3.2026 13:00:00 EEST | Pressmeddelande

Den ekonomiska tillväxten i Ryssland saktade in till 1 % under 2025. Framför allt den svagare utvecklingen i den privata konsumtionen och i fasta investeringar hämmade den ekonomiska tillväxten, då inkomstökningen mattades av, skattebördan växte och räntorna låg på en hög nivå. Nettoexportens bidrag till BNP-tillväxten var negativt 2025. Rysslands export tyngdes i fjol särskilt av de nya sanktionerna mot oljebranschen

BOFIT-ennuste: Venäjän talouskasvu edellisvuoden tasolla vuonna 202630.3.2026 13:00:00 EEST | Tiedote

Venäjän talouden kasvu hidastui vuoden 2025 aikana yhteen prosenttiin. Erityisesti yksityisen kulutuksen ja kiinteiden investointien aiempaa heikompi kehitys vaimensi talouskasvua, kun palkkatulojen kasvu hidastui, verorasitus kasvoi ja korkotaso oli korkea. Vuonna 2025 nettoviennin vaikutus bruttokansantuotteen kasvuun oli negatiivinen. Vientiä painoivat viime vuonna varsinkin uudet öljysektorin pakotteet.

BOFIT Forecast for Russia 2026–2028: Economic growth at last year’s level in 202630.3.2026 13:00:00 EEST | Press release

Russia’s economic growth last year slowed to 1 percent. Particularly weak trends in private consumption and fixed investment dragged down growth following decelerated wage growth, an increased tax burden and high interest rates. Net exports had a negative impact on GDP growth in 2025. Russian exports last year were hit hard by new sanctions on the oil sector.

Bostadslånens återbetalningstider har blivit längre27.3.2026 10:00:00 EET | Pressmeddelande

Den genomsnittliga återbetalningstiden för nya bostadslån har förlängts i ett år. Betalningstiderna har förlängts framför allt för ägarbostadslån. I en del av bostadslånen kan också räntejusteringar inverka på den slutliga återbetalningstiden för lånet.

Asuntolainojen takaisinmaksuajat ovat pidentyneet27.3.2026 10:00:00 EET | Tiedote

Uusien asuntolainojen keskimääräinen takaisinmaksuaika on pidentynyt vuoden ajan. Maksuajat ovat pidentyneet etenkin omistusasumiseen otetuissa lainoissa. Osassa asuntolainoista myös korontarkistus voi vaikuttaa lainan lopulliseen takaisinmaksuaikaan.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom