Households’ investment fund holdings increased in 2024

10.2.2025 10:00:00 EET | Suomen Pankki | Press release

In 2024, Finnish households invested a further EUR 1.6 billion in net terms in Finnish investment funds[1]. Equity funds attracted clearly the largest investments (EUR 1.0 billion), followed by bond funds (EUR 500 million). Of the fund types, only real estate funds recorded more redemptions than new investments, totalling EUR 240 million, on net.

In addition to new investments, the value of domestic investment fund holdings also appreciated by over EUR 3 billion in 2024. At the end of 2024, households’ holdings in domestic investment funds totalled EUR 38.7 billion. Households also had a significant amount of holdings (estimated at EUR 25.1 billion[2]) in domestic investment funds through unit-linked insurance policies.

In 2024, Finnish households also invested a further EUR 1.2 billion in foreign investment funds[3], and the value of these holdings appreciated by EUR 1.0 billion. At the end of 2024, foreign investment fund units held by households amounted to EUR 8.6 billion, compared with EUR 6.5 billion a year earlier. Households also had holdings in foreign investment funds (estimated at EUR 10.5 billion) through unit-linked insurance policies.

Foreign equities held by Finnish households outperformed domestic equities in 2024

At the end of 2024, households owned listed equities[4] worth EUR 46.5 billion, an increase of 1% year-on-year. Most (85%) of the listed equities held by households were domestic companies’ equities. However, the proportion of foreign equities has increased. At the end of 2024, foreign equities accounted for 15% of households’ holdings of listed equities, as opposed to 13% a year earlier. In 2024, households invested a further EUR 1.6 billion in net terms[5] in listed equities.

The rate of return[6] on domestic companies’ equities held by households was zero in 2024. The return on foreign companies’ equities was 18%. In 2024, households received dividends worth EUR 1.9 billion from Finnish companies, but the value of domestic equities declined by almost an equal amount. The value of foreign equity holdings increased in turn by EUR 0.9 billion in 2024, and households’ dividends from foreign companies totalled EUR 170 million.

Interest rates on deposits with agreed maturity and investment deposits have declined

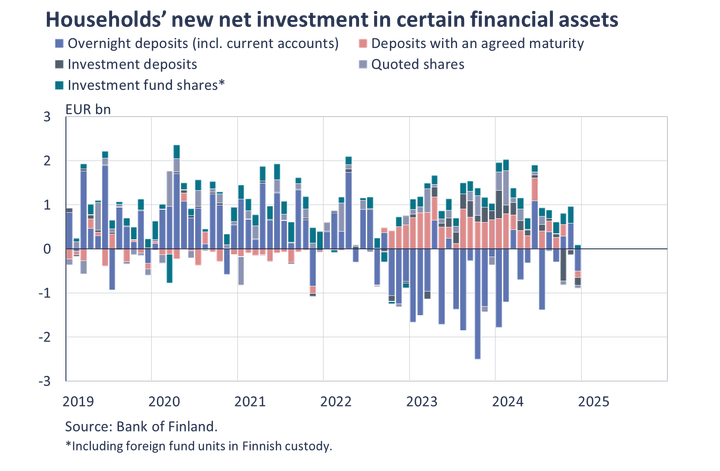

At the end of 2024, the stock of Finnish households’ deposits stood at EUR 110.2 billion, and the annual growth rate of the deposit stock was 1.4%. Over the year, households moved EUR 4.9 billion of their funds to higher-interest deposit accounts. This was notably less than in the previous year, when the corresponding inflows totalled EUR 9.3 billion. At the end of 2024, 61% of households’ assets on deposit accounts were on overnight deposit accounts (incl. current accounts), 14% were deposits with an agreed maturity and 25% were investment deposits[7].

The average interest rate on the deposit stock started to decline in 2024, standing at 1.23% in December. The average interest rate on the stock of deposits with an agreed maturity fell below 3% in December, while that on the stock of investment deposits fell below 2%. The average interest rate on new deposit agreements with an agreed maturity stood at 2.79% in December 2024, compared with 3.42% in December a year earlier.

For further information:

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi

Ville Tolkki, tel. +358 9 183 2420, email: ville.tolkki(at)bof.fi

Related statistical data and graphs are also available on the Bank of Finland website at: https://www.suomenpankki.fi/en/statistics/?epslanguage=en.

The next news release on saving and investing will be published at 10:00 on 8 May 2025.

[1] Including UCITS and non-UCITS investment funds registered in Finland.

[2] At the end of September 2024. The estimate is calculated based on Finance Finland’s insurance savings statistics and the Bank of Finland’s statistics on insurance corporations.

[3] Investment fund units held in custody in Finland.

[4] Held in custody in Finland.

[5] Purchases – sales.

[6] The return has been calculated from revaluation adjustments based on monthly changes in equity prices and dividends received.

[7] Investment deposits are deposits redeemable at notice. They do not have a fixed maturity date (unlike deposits with an agreed maturity), but have a notice period, during which the deposits cannot be converted into cash without consequences (unlike overnight deposits). This category also includes investment accounts without a period of notice or agreed maturity but which have restrictive drawing provisions.

Links

Bank of Finland

The Bank of Finland is the national monetary authority and central bank of Finland. At the same time, it is also a part of the Eurosystem, which is responsible for monetary policy and other central bank tasks in the euro area and administers use of the world’s second largest currency – the euro.

Alternative languages

Subscribe to releases from Suomen Pankki

Subscribe to all the latest releases from Suomen Pankki by registering your e-mail address below. You can unsubscribe at any time.

Latest releases from Suomen Pankki

Eurosystemets penningpolitiska beslut19.3.2026 15:22:31 EET | Pressmeddelande

ECB-rådet beslutar om penningpolitiken i euroområdet. ECB-rådet beslutade idag att hålla de tre styrräntorna oförändrade.

EKP:n rahapoliittisia päätöksiä19.3.2026 15:22:31 EET | Tiedote

EKP:n neuvosto päättää euroalueen rahapolitiikasta. EKP:n neuvosto päätti tänään pitää EKP:n kolme ohjauskorkoa ennallaan.

Medialle: Suomen Pankki julkaisee Suomen talouden väliennusteen ti 24.3. klo 7.0019.3.2026 13:29:36 EET | Kutsu

Suomen Pankki julkaisee Suomen talouden väliennusteen tiistaina 24.3.2026 klo 7.00. Väliennuste julkaistaan osoitteessa www.eurojatalous.fi. Ennuste on saatavilla embargolla maanantaina 23.3. n. klo 15.00. Ilmoittaudu ennusteen embargojakeluun viimeistään maanantaina 23.3. klo 12.00. Ilmoittaudu embargojakelulistalle Väliennusteen julkaisun yhteydessä ei järjestetä erillistä tiedotustilaisuutta. Asiantuntijamme ovat tiedotusvälineiden käytettävissä. Haastattelupyynnöt pyydetään osoittamaan Suomen Pankin viestinnälle (media@bof.fi, p. 09 183 2101). Suomen Pankki julkaisee Suomen talouden väliennusteen kaksi kertaa vuodessa. Keväällä ja syksyllä julkaistavissa väliennusteissa päivitetään Suomen talouden näkymät talouskasvun, työllisyyden ja inflaation osalta. Laajemmat Suomen talouden ennustejulkaisut ilmestyvät kesä- ja joulukuussa. Kesäkuun ennuste julkaistaan 12.6.2026.

Räntan på centralbanksinlåningen tyngde Finlands Banks verksamhetsresultat också 202513.3.2026 11:00:00 EET | Pressmeddelande

Bankfullmäktige har i dag fastställt Finlands Banks bokslut på framställning av Finlands Banks direktion. Finlands Banks reviderade resultat för räkenskapsåret 2025 är liksom föregående år noll euro efter upplösning av avsättningar. Verksamhetsresultatet för 2025 var −215 miljoner euro (−1 027 miljoner euro 2024) och det täcktes genom upplösning av den generella avsättningen.

Keskuspankkitalletuksille maksetut korot painoivat Suomen Pankin toiminnallista tulosta myös vuonna 202513.3.2026 11:00:00 EET | Tiedote

Pankkivaltuusto on tänään vahvistanut Suomen Pankin tilinpäätöksen Suomen Pankin johtokunnan esityksestä. Suomen Pankin tilintarkastettu tulos tilikaudelta 2025 on varausten purkamisen jälkeen nolla euroa edellisvuoden tavoin. Vuoden 2025 toiminnallinen tulos oli –215 milj. euroa (–1 027 milj. euroa vuonna 2024), ja se katettiin purkamalla reaaliarvovarausta.

In our pressroom you can read all our latest releases, find our press contacts, images, documents and other relevant information about us.

Visit our pressroom